They say numbers don’t lie. If that be the case, one message of truth shines through in the inventory figures below when compared to the ones I calculated exactly nine months earlier for Miami-Dade County condos: sales up, supply down. I compiled the figures below on April 22, 2010 from the MLS in the exact same manner as I had the night of July 23, 2009. Below, you will find three sets of spreadsheets and graphs: the first pertaining to the inventory of condos throughout Miami-Dade County; the second to those residing only in Miami while the third concentrates on those residing in Miami Beach.

Once again, I divided the supply figures into seven price ranges and included only sales that have closed within the past six months. The last three columns show the percentage change in those statistics when compared to those published nine months earlier for July 2009. It should be rather apparent, with a few exceptions, that the overall pattern is that condo inventory has decreased and closed sales have increased quite considerably within the past nine months. For example, overall condo inventory in Miami-Dade County has decreased 13.78 percent while closed sales have increased 19.23 percent during that time frame which led to a 27.69 percent decrease in the overall months of supply.

The figures in the images below may be a bit difficult to read so I also published the workbook for this month’s Miami & Miami Beach Condo Trends in its entirety. Be sure to check it out. The worksheet and graph tabs can be found along the bottom of the workbook.

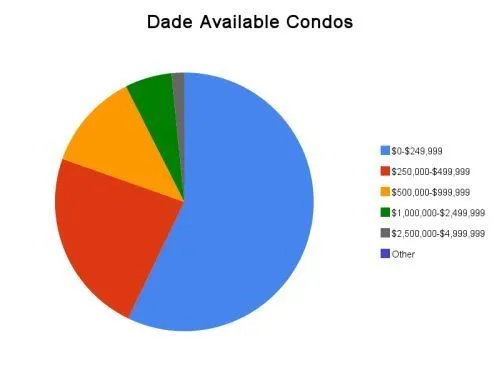

Below, you will find the Miami-Dade County condo supply and sales figures for April 2010:

The following statistics encompass only those condos located throughout Miami (not other areas of Dade County such as Miami Beach, Aventura, Sunny Isles Beach, etc.):

The following statistics encompass only those condos located throughout Miami Beach:

Market pessimists will likely argue that the statistics above do not incorporate developer inventory. Commonly known as shadow inventory, developer inventory is typically not recorded in the MLS. However, these people need to bear in mind that closed developer sales also are not included in the figures above. Obviously, shadow inventory was a bigger problem nine months ago than it is today. A more valid argument should point to the home buyer tax credit being the catalyst that increased sales within the past nine months. Personally, however, I feel that the the home buyer tax credit has had a greater impact on the single family home market than the condo market. It has played a very insignificant role in our business and I have spoken to other real estate agents who specialize in condominiums who have encountered the same. With the home buyer tax credit expiring this Friday, we should be able to see within the next three months how instrumental of a role it has played in the increased sales numbers we’ve witnessed.

Leave a Reply